FinTech in the Philippines Booms in 2019

Take a look at your wallet or purse right now because you might see less of it in the future. That’s what the Bangko Sentral ng Pilipinas or Central Bank of the Philippines (BSP) hopes, at least. Financial Technology (FinTech) has been on the rise in the Philippines and the rest of Southeast Asia. Electronic wallet or e-wallet services like Gcash, GrabPay, and Paymaya have made it easy for Filipinos to go cashless on routine transactions.

E-What?

This isn’t anything new. E-wallet services like Gcash have been around since 2004, but it didn’t take off. Though the country was already making and breaking records for texting, not everyone had a phone yet and barely anyone had a smartphone. For reference, the first iPhone wouldn’t be released for another 3 years.

High mobile device usage in the Philippines gives E-wallet services a rich market available to them. (Statistics from: https://internetworldstats.com/asia.htm#ph)

High mobile device usage in the Philippines gives E-wallet services a rich market available to them. (Statistics from: https://internetworldstats.com/asia.htm#ph)

Since its conception, The BSP has had a problem with the unbanked – the population who don’t maintain a bank account. In the Philippines, only 22% of adults have a bank account. The other 78% feel that they don’t have enough money for an account, they lack required documents, and most of all, a lot of Filipinos just believe they don’t need a bank account. Being unbanked means their only option for transactions is physical cash which in turn severely limits economic growth. It also comes with a lot of risks, money can get lost or stolen; counting takes time and you run a margin of error; if your savings are in one place they could fall damage to weather or pests.

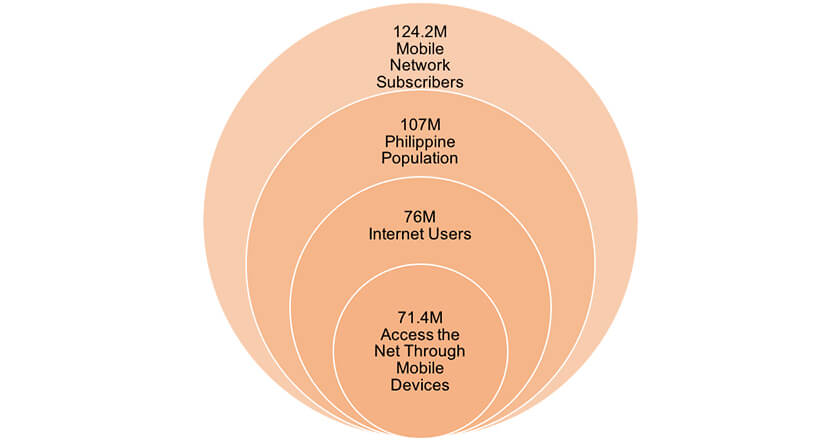

The good news for the BSP is that, as of writing, the Philippines has a population of 107 million with a total of 124.2 million mobile network subscriptions. Meanwhile, internet usage sits at 76 million with 71.4 million accessing the web through mobile devices. This means almost three-quarters of the population have access to the internet and mobile devices. The country has been sitting on a goldmine of FinTech opportunity.

Enter the NRPS

To help answer the BSP’s problem, they established the National Retail Payment System (NRPS). The NRPS was established in 2013 and by 2020, they want 20% of all payment transactions electronic. Through digital payments, transactions are quicker, safer, and more efficient. For example, users don’t have to wait in line to pay bills. In fact, they can automate bill payments. There is no danger of misplacing or getting money stolen if you don’t carry it in the first place. There’s no danger of getting or giving the wrong amount of change because people can pay the exact amount.

Benefits like this have long been available to credit card holders. But out of the 22% of adults that have bank accounts, only 9% of them have credit cards. For E-wallet services, this is a godsend, this means there isn’t much to worry about competition. They might be right too, as of 2019, there are already more e-wallet users than there are credit card holders. The Philippines isn’t alone in this, either the same situation can be found in Thailand, Indonesia, and the rest of Southeast Asia.

Uphill Climb

Aside from paying bills, e-wallets also make it easier for people to save their money. Banks have been tying up with e-wallet services to make it easier to open accounts using the credentials already in hand. It also makes it easier for people to spend their money. E-wallets introduce users to a wider range of both products & services and customers or what the BSP refers to as Financial Inclusion – a chance for the disenfranchised to be afforded the same things more privileged citizens get. Small to medium-sized enterprises (SMEs) can now open themselves to wider markets without having to scramble for payment options.

The BSP has no intentions nor dreams of e-wallets replacing physical cash. Regular e-wallet transactions right now are limited to bill payments, online shopping, and other small-ticket items. But in a future with a FinTech enabled population, employers can distribute salaries through e-wallets, travelers can spend money here & overseas without hassle, and OFWs can send remittances to their families easier.

A few problems still need to be addressed, however. While the country ranks the highest in internet usage, it also ranks among the lowest in internet speed. The stability of connections also fall into question. In social media, users are airing out customer service woes. When money is involved, concerns like these beg to be resolved.

There’s a bright future for FinTech in the Philippines. It’s a whole system that could succeed where traditional banking failed.

Share your e-wallet stories with us on Facebook, Twitter, Instagram, or email us at info@